The number 1 question I’m always asked when it come to claiming Social Security is “When should I claim my benefits?” My answer is simply “What’s your check out date?” or a better follow-up question is “what is yours and your spouses Joint Check out dates?” Since the surviving spouse inherits the greater of the two benefits, its of utmost importance if longevity runs in either side of the family to have the higher earning spouse delay until 70 before claiming.

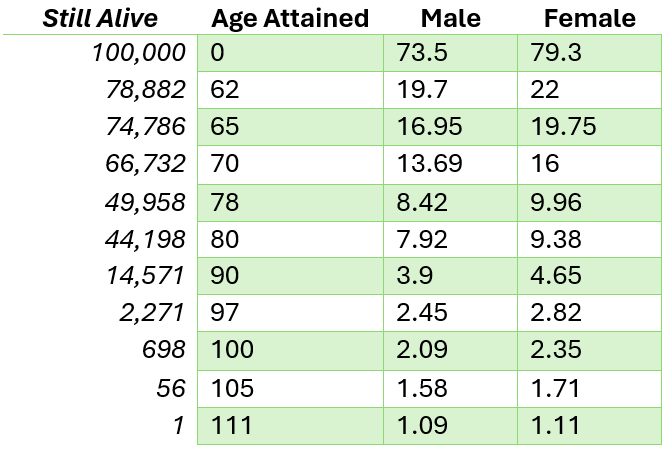

2021 SSA Trustee Actuarial Life Expectancy Table

What Can We Learn from Table Above

The Longer You Live the Longer You Live!

At Age 78 approximately 50% are still alive!

Are you above average or below average?

What % of college graduates, graduate in the bottom half of their class?

Are you an Optimist or a Pessimist?

My mother passed away last year at age 97! What’s Your Family History?

No Trade In’s – are you taking care of your vehicle?

Those Living with Purpose tend to live longer than those without!

3 Truths in Life

- The Only Certainty is Uncertainty

- Life is Not Fair

- You have to Deal with the Hand Your Dealt

Once you decide to retire, you must deal with a number of Known & Unknown RISKS! There is Inflation Risk, Market Risk, Interest Rate Risk, Tax Risk, Loss of a Spouse Risk, Health Risk, Etc. Etc. But I feel the #1 Risk in Retirement is LONGEVITY RISK! The most difficult variable for any financial planner is determining how long the money must last! Many corporations eliminated their Defined Benefit Plans over the last 30 years because they didn’t want to liability of dealing with the Longevity Risk. Many cities and states are dealing with greatly unfunded pension liabilities.

Social Security will be facing similar challenges in the next decade and eventually Congress will decide to deal with it, thru changes similar to what transpired back in 1983. They increased FICA tax rates and the amount of income subject to FICA taxes, they changed the Full Retirement Age from 65 to 66 – 67. The changes did not affect those currently receiving benefits or those over 55 years of age and were phased in over 20 years.

Lifetime Guaranteed Income

The beauty of Social Security – a Pension – an Annuity is that they will pay you a monthly check for as long as you live! I look at and treat Social Security benefits as a bond or fixed income security that will pay myself and my wife a check for as long as we live. I call it My Longevity Insurance policy.

The main issue that I continually harp upon is making sure you and your clients make an informed decision as to when to claim benefits. Remember whatever your check is at age 62 it is DOUBLE at age 70! If you start at age 62 and I start at age 70, you will receive 8 years of checks before I start, but I will catch you around age 80.

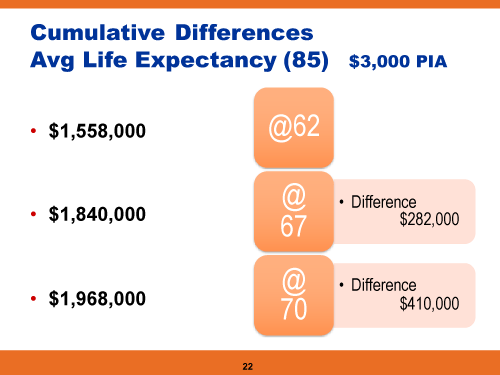

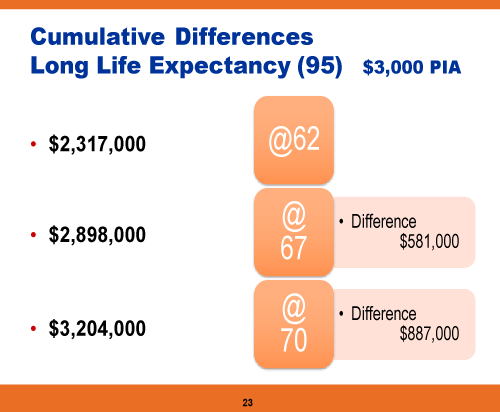

The Slides below show the Cumulative Difference in Social Security Benefits of an individual claiming at 62 vs 67 vs 70, assuming a $3,000 per month PIA (check at FRA), a similar age spouse you didn’t work and collected spousal benefit at same time and a 2% COLA.

![]()

Happy Spring and remember, I’m always here for you and your clients.

David P. Zander

CFP Emeritus Board ™

dzander@back9pro.com

260-615-0078